January may be turning icy 🥶🌨 but Buyers are heating up. 🔥 These two homes are pending with amazing… smart .. 1st time home buyers!! Who’s ready to take advantage of some new lower rates before more buyers jump into the competition? 🏘 #SmartHomeBuying #buildgenerationalwealth

This fan is a practical and robust solution for beating the summer heat while optimizing space. Do you need help with adapting this text, or would you like it tailored further for a specific purpose?

This fan is an effective solution for summer heat and space efficiency. As an affiliate, I found it invaluable for our camp in Mississippi, providing excellent airflow and cooling. Its easy installation and three-speed functionality make it a highly satisfying buy for combating high temperatures.

Picture does not represent the actual fan but is of similar size. Click here for fan details

The Vent Cleaner is a crucial device designed to remove lint from difficult-to-access spaces. It easily connects to any vacuum cleaner nozzle. This allows for the efficient extraction of trapped lint at the bottom of your filter. This tool addresses a widespread problem that many individuals face, ensuring improved vacuum performance and maintenance. The Vent Cleaner is practical. It offers a simple solution to an often-overlooked task. It ultimately enhances the cleaning process and extends the life of your vacuum cleaner. With its easy attachment and effective design, this tool simplifies an essential household chore. This device can be used in your shop vac as well and will help with many household cleaning problems. Dust Daisy’s long 33″ non-clog hose can easily reach all your hard to access areas. As an Amazon Affiliate I look for top quality home solution products for my clients.

A dehumidifier is a device that removes moisture from the air to maintain an optimal level of humidity indoors. By reducing humidity, it helps prevent issues like mold, mildew, and dust mites, which thrive in damp environments. This can be particularly beneficial for people with allergies, asthma, or respiratory sensitivities.

How a Dehumidifier Works:

Air Intake: The device pulls in humid air from the room.

Cooling Coil: The air passes over cold coils, which cools the air and condenses the moisture into liquid form.

Water Collection: The condensed moisture collects in a reservoir or drains away.

Warm Air Release: Drier air is then reheated and released back into the room.

This is a great addition to my home that I didn’t know I needed. It’s improved the air quality of each room and adds comfort and functionality. Great buy and has given me peace of mind. https://amzn.to/4g7xFm9

Benefits of Using a Dehumidifier:

Reduces humidity, making the air feel cooler and more comfortable.

Helps prevent mold, mildew, and other moisture-related issues.

Improves air quality by reducing allergens and odors.

Protects furniture, electronics, and building structures from moisture damage.

Most dehumidifiers have features like adjustable humidity settings, auto shut-off, and continuous drainage options for convenience.

The time it takes to close on a home can vary depending on several factors, including the specific circumstances of the home purchase and the parties involved. On average, it typically takes around 30 to 45 days to close on a home after the purchase agreement is signed. However, it’s important to note that this is just an estimate, and the actual timeline can be shorter or longer depending on various factors, such as:

Mortgage Financing: If you’re obtaining a mortgage to purchase the home, the timeline can be influenced by factors such as the lender’s efficiency, the complexity of the loan application, and any potential delays in obtaining the necessary documentation or appraisal.

Home Inspection and Appraisal: The time it takes to schedule and complete a home inspection and appraisal can impact the closing timeline. If any issues or discrepancies are found during these processes, it may require additional negotiations or repairs, which can extend the closing timeframe.

Title Search and Insurance: A title search is typically conducted to ensure there are no outstanding liens or claims on the property. This process can take a few weeks, and obtaining title insurance may also be necessary, which can add additional time.

Contingencies and Negotiations: The presence of contingencies in the purchase agreement, such as a home sale contingency or repairs requested by the buyer, can affect the closing timeline. If negotiations or resolutions are required, it may lengthen the closing process.

Local Factors and Seasonal Variations: The time required to close on a home can vary depending on local customs, regulations, and the workload of the professionals involved, such as real estate agents, lenders, and attorneys. Additionally, certain seasons or times of the year, such as holidays or peak buying seasons, can result in increased demand and potentially longer closing times.

It’s essential to work closely with your real estate agent, lender, and other professionals involved in the process to get a more accurate estimate of the closing timeline for your specific situation.

If you’re planning to buy a home, one thing to consider is what experts project home prices will do in the future and how that might affect your investment. While you may have seen negative news over the past year about home prices, they’re doing far better than expected and are rising across the country. And data shows, experts forecast home prices will keep appreciating.

Experts Project Ongoing Appreciation

Pulsenomics polled over 100 economists, investment strategists, and housing market analysts in the latest quarterly Home Price Expectation Survey (HPES). The results show what the panelists project will happen with home prices over the next five years. Here are those expert forecasts saying home prices will go up every year through 2027 (see graph below):If you’re someone who was worried home prices would fall because of stories you’ve read online, here’s the big takeaway. Even though home prices vary by local market, experts project prices will continue to rise across the country for years to come. And these numbers indicate the return to more normal home price appreciation.

And while the projected increase in 2024 isn’t as large as 2023, it’s important to recognize home price appreciation is cumulative. In other words, if these experts are correct, after your home’s value rises by 3.32% this year, it’ll appreciate by another 2.17% next year. This is a good example of why owning a home is a choice that wins big over time.

What Does This Mean for You?

Once you buy a home, price appreciation raises your home’s value, and that grows your household wealth. To see how a typical home’s value could change in the next few years using the expert projections from the HPES, check out the graph below:In this example, let’s say you bought a $400,000 home at the beginning of this year. If you factor in the forecast from the HPES, you could potentially accumulate more than $71,000 in household wealth over the next five years.

So, if you’re thinking about whether buying a home is a good choice, remember how it can be a powerful way to grow your wealth in the long run.

Bottom Line

According to the experts, home prices are expected to grow over the next five years at a more normal pace. If you’re ready to become a homeowner, know that buying today can set you up for long-term success as home values (and your own net worth) grow. Let’s connect to start the home buying process today.

If you’re reading headlines about inflation or mortgage rates, you may see something about the recent decision from the Federal Reserve (the Fed). But what does it mean for you, the housing market, and your plans to buy a home? Here’s what you need to know.

Inflation and the Housing Market

While the Fed’s working hard to lower inflation, the latest data shows that, while the number has improved some, the inflation rate is still higher than the target (2%). That played a role in the Fed’s decision to raise the Federal Funds Rate last week. As Bankrateexplains:

“Keeping its inflation-fighting streak alive, the Federal Reserve has raised interest rates for the 10th time in 10 meetings . . . The hikes aimed to cool an economy that was on fire after rebounding from the coronavirus recession of 2020.”

While the Fed’s actions don’t directly dictate what happens with mortgage rates, their decisions do have an impact and contributed to the intentional cooldown in the housing market last year.

How This Impacts You

During times of high inflation, your everyday expenses go up. That means you’ve likely felt the pinch at the gas pump and in the grocery store. By raising the Federal Funds Rate, the Fed is actively trying to lower inflation. If the Fed is successful, it could also ultimately lead to lower mortgage rates and better homebuying affordability for you. That’s because when inflation is high, mortgage rates tend to be high. But, as inflation cools, experts say mortgage rates will likely fall.

Where Experts Think Mortgage Rates and Inflation Will Go from Here

Moving forward, both inflation and mortgage rates will continue to impact the housing market. And as Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Mortgage rates are likely to descend lower later in the year as the consumer price inflation calms down . . .”

Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), explains:

“We continue to expect that mortgage rates will drift down over the course of the year as the economy slows . . .”

While there’s no way to say with certainty where mortgage rates will go from here, the experts think mortgage rates will trend down this year if inflation comes down too. To stay informed on the latest insights, connect with a trusted real estate advisor. They keep their pulse on what’s happening today and help you understand what the experts are projecting and how it could impact your homeownership plans.

Bottom Line

Don’t let headlines about the latest decision from the Fed confuse you. Where mortgage rates go from here depends on what happens with inflation. If inflation cools, mortgage rates should tick down as a result. Let’s connect so you have expert insights on housing market changes and what they mean for you.

If you’re a homeowner thinking about making a move, you may wonder if it’s still a good time to sell your house. Here’s the good news. Even with higher mortgage rates, buyer traffic is actually picking up speed.

Data from the latest ShowingTime Showing Index, which is a measure of buyers actively touring homes, helps paint the picture of how much buyer demand has increased in recent months (see graph below):

As the graph shows, the first two months of 2023 saw a noticeable increase in buyer traffic. That’s likely because the limited number of homes for sale kept shoppers looking for homes even during colder months.

To help tell the story of why the latest report is significant, let’s compare foot traffic this February with each February for the last six years (see graph below). It shows this was one of the best Februarys for buyer activity we’ve seen in recent memory.

In the last six years, we saw the most February buyer traffic in 2021 and 2022 (shown in green above), but those years were highly unusual for the housing market. So, if we compare February 2023 with the more normal, pre-pandemic years, data shows this year still marks a clear rise in buyer activity.

The uptick in buyer traffic is even more noteworthy considering the increase in mortgage rates this February. The Freddie Mac 30-year fixed mortgage rate rose from 6.09% during the week of February 2nd to 6.50% in the week of February 23rd. But even with higher rates, more buyers were looking for a home.

Jeff Tucker, Senior Economist at Zillow, says the increased buyer activity could continue:

“More buyers will keep coming out of the woodwork. We always see a seasonal uptick in home shoppers in March and April . . .”

If you’re looking to sell your house, seeing buyers still active in the market this year should be encouraging. It’s a sign buyers are out there and could be looking for a home just like yours. Working with a real estate professional to list your house now will help you get your home in front of eager buyers today.

Bottom Line

Rising foot traffic is a bright spot for this year’s housing market and indicates that buyers are looking to purchase this year, even with higher mortgage rates. If you’re ready to sell your house, let’s connect.

If you’re planning to buy a home, an inspection is an important step in the process. It assesses the condition of the home before you finalize the transaction. It’s also a different step in the process from an appraisal, which is a professional evaluation of the market value of the home you’d like to buy. In most cases, an appraisal is ordered by the lender to confirm or verify the value of the home prior to lending a buyer money for the purchase. Here’s the breakdown of each one and why they’re both important when buying a home.

Home Inspection

Here’s the key difference between an inspection and an appraisal. Bankratesays:

“In short, while an appraisal helps you understand a home’s value, inspections help you understand a home’s condition.”

The home inspection is a way to determine the current state, safety, and condition of the home before you finalize the sale. If anything is questionable in the inspection process – like the age of the roof, the state of the HVAC system, or just about anything else – you as a buyer have the option to discuss and negotiate any potential issues or repairs with the seller before the transaction is final. Your real estate agent is a key expert to help you through this part of the process.

Home Appraisal

The National Association of Realtors (NAR) explains:

“A home purchase is typically the largest investment someone will make. Protect yourself by getting your investment appraised! An appraiser will observe the property, analyze the data, and report their findings to their client. For the typical home purchase transaction, the lender usually orders the appraisal to assist in the lender’s decision to provide funds for a mortgage.”

When you apply for a mortgage, an unbiased appraisal (which is required by the lender) is the best way to confirm the value of the home based on the sale price. Regardless of what you’re willing to pay for a house, if you’ll be using a mortgage to fund your purchase, the appraisal will help make sure the bank doesn’t loan you more than what the home is worth.

This is especially critical in today’s sellers’ market where low inventory is driving an increase in bidding wars, which can push home prices upward. When sellers are in a strong position like this, they tend to believe they can set whatever price they want for their house under the assumption that competing buyers will be willing to pay more.

However, the lender will only allow the buyer to borrow based on the value of the home. This is what helps keep home prices in check. If there’s ever any confusion or discrepancy between the appraisal and the sale price, your trusted real estate professional will help you navigate any additional negotiations in the buying process.

Bottom Line

The inspection and the appraisal are critical steps when buying a home, and you don’t need to manage them by yourself. Let’s connect today so you have the expert guidance you need to navigate the entire homebuying process.

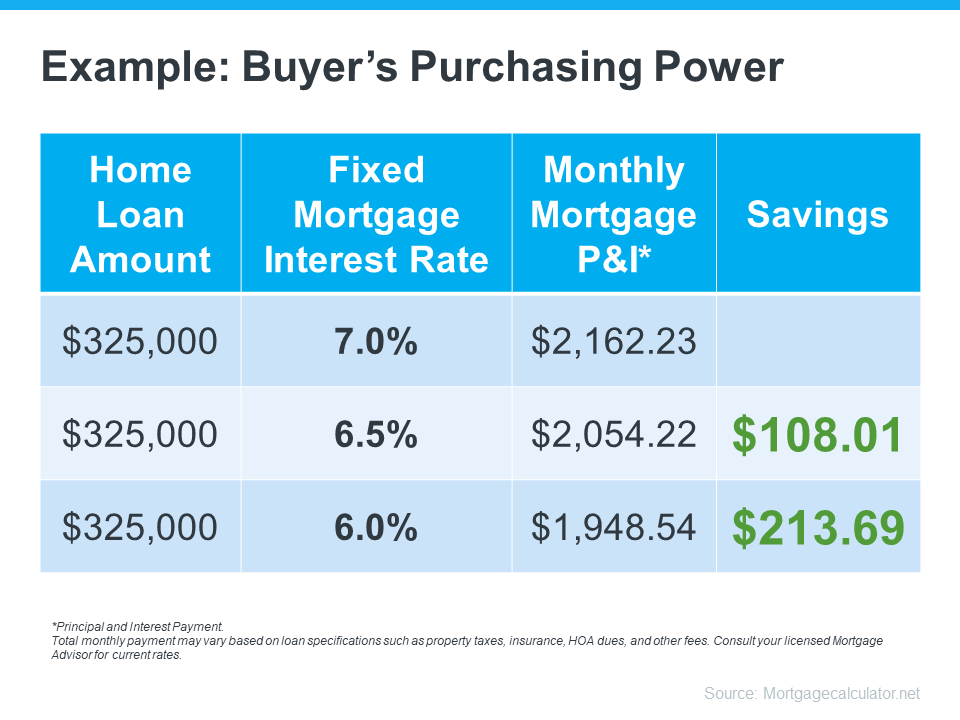

The 30-year fixed mortgage rate has been bouncing between 6% and 7% this year. If you’ve been on the fence about whether to buy a home or not, it’s helpful to know exactly how a 1%, or even a 0.5%, mortgage rate shift affects your purchasing power.

The chart below helps show the general relationship between mortgage rates and a typical monthly mortgage payment:

Even a 0.5% change can have a big impact on your monthly payment. And since rates have been moving between 6% and 7% for a while now, you can see how it impacts your purchasing power as rates go down.

What This Means for You

You may be tempted to put your homebuying plans on hold in hopes that rates will fall. But that can be risky. No one knows for sure where rates will go from here, and trying to time them for your benefit is tough. Lisa Sturtevant, Housing Economist at Bright MLS, explains:

“It is typically a fool’s errand for a homebuyer to try to time rates in this market . . . But volatility in mortgage rates right now can have a real impact on buyers’ monthly payments.”

That’s why it’s critical to lean on your expert real estate advisors to explore your mortgage options, understand what impacts mortgage rates, and plan your homebuying budget around today’s volatility. They’ll also be able to offer advice tailored to your specific situation and goals, so you have what you need to make an informed decision.

Bottom Line

Your ability to buy a home could be impacted by changing mortgage rates. If you’re thinking about making a move, let’s connect so you have a strong plan in place.