A dehumidifier is a device that removes moisture from the air to maintain an optimal level of humidity indoors. By reducing humidity, it helps prevent issues like mold, mildew, and dust mites, which thrive in damp environments. This can be particularly beneficial for people with allergies, asthma, or respiratory sensitivities.

How a Dehumidifier Works:

Air Intake: The device pulls in humid air from the room.

Cooling Coil: The air passes over cold coils, which cools the air and condenses the moisture into liquid form.

Water Collection: The condensed moisture collects in a reservoir or drains away.

Warm Air Release: Drier air is then reheated and released back into the room.

This is a great addition to my home that I didn’t know I needed. It’s improved the air quality of each room and adds comfort and functionality. Great buy and has given me peace of mind. https://amzn.to/4g7xFm9

Benefits of Using a Dehumidifier:

Reduces humidity, making the air feel cooler and more comfortable.

Helps prevent mold, mildew, and other moisture-related issues.

Improves air quality by reducing allergens and odors.

Protects furniture, electronics, and building structures from moisture damage.

Most dehumidifiers have features like adjustable humidity settings, auto shut-off, and continuous drainage options for convenience.

If buying or selling a home is part of your dreams for 2023, it’s essential for you to understand today’s housing market, define your goals, and work with industry experts to bring your homeownership vision for the new year into focus.

In the last year, high inflation had a big impact on the economy, the housing market, and likely on your wallet too. That’s why it’s critical to have a clear understanding of not just the market today, but also what you want out of it when you buy or sell a home. Danielle Hale, Chief Economist at realtor.com, explains:

“The key to making a good decision in this challenging housing market is to be laser focused on what you need now and in the years ahead, so that you can stay in your home long enough that buying is a sound financial decision.”

Here are a few questions you can start thinking through as you fine tune your goals for 2023.

1. What’s Motivating You?

You’re dreaming about making a move for a reason – what is it? No matter what’s happening in the market, there are still many compelling reasons to buy a home today. Your needs may have changed in a way your current house can’t address, or you could be ready to step into homeownership for the first time and have a space that’s truly your own. Use what’s motivating you as a guidepost in partnership with an expert advisor to help make sure your move will give you a lasting sense of accomplishment.

2. What Does Your Next Home Look Like?

You know you want to move, but how would you describe your dream home? The available supply of homes for sale has grown, and that could mean more options to choose from when you buy. Just be sure to keep your budget in mind and work with a trusted real estate professional to balance your wants and needs. The better you understand what’s essential and where you can be flexible, the easier it can be to find the home that’s right for you.

3. How Ready Are You To Buy?

Getting clear on your budget and savings is essential before you get too far into the process. Working with a local agent and a lender early is the best way to make sure you’re in a good position to buy. This could include planning how much to save for a down payment, getting pre-approved for a home loan, and assessing your current home equity if your move involves selling your existing house.

A Professional Will Guide You Through Every Step of the Process

Buying or selling a home is a big process that takes expertise to navigate. If that feels a bit overwhelming, you aren’t alone. According to a recent Harris Pollsurvey, one in five respondents see a lack of information or knowledge about the homebuying process as a barrier from owning a home. Don’t let uncertainty hold you back from your goals this year. A trusted expert can bridge that gap and give you the best advice and information about today’s market.

Bottom Line

Let’s connect to plan how your dreams for 2023 can become a reality.

Acquisition Debt is the amount of money borrowed used to buy, build or improve a principal residence or second home. Under the new tax law, mortgages taken after 12/14/17 are limited to a combination of $750,000 on the first and second homes. The mortgage interest on this debt is tax deductible when itemizing deductions.

It is a dynamic number that is reduced with each payment as the unpaid balance goes down. The only way to increase acquisition debt is to borrow money to make capital improvements.

Prior to the new law, homeowners could additionally borrow up to $100,000 of home equity debt for any purpose and deduct the interest when itemizing deductions. Mortgage interest on home equity debt is no longer deductible unless it is for capital improvements.

Acquisition debt cannot be increased by refinancing. Some confusion occurs because mortgage lenders are concerned in making home loans that will be repaid according the terms of the note and using the home as collateral. That does not include making a tax-deductible mortgage.

Another thing that adds confusion to the issue is that the lenders will annually report how much interest was paid in a year but only the amount that is attributable to acquisition debt is deductible.

Even if the interest on the cash-out refinance is not deductible, it may be advantageous to pay off higher interest debt such as credit card debt and replacing it with lower mortgage debt.

It is the responsibility of the taxpayer to know what part of their mortgage debt is deductible. The challenge becomes more difficult after a cash-out refinance. Homeowners should keep records of all financing and capital improvements and consult with their tax professional.

A home that isn’t being maintained like others in the neighborhood can negatively affect your visual sense of appeal and in some extreme cases, even affect property values. It might be an overgrown yard, a fence in need of repair, excessive noise, unruly pets, paint peeling on the home or even a car or boat parked in front of the home that hasn’t moved in weeks.

Most people want to be good neighbors and may be willing to correct an issue once it is brought to their attention. A practical but possibly, confrontational solution is to contact the responsible person and describe your perception of the issue. However, they may not always agree with the same urgency and it might be necessary to seek other remedies.

An owner-occupant may be more sympathetic to the neighbors and willing to correct the issue. If you think the home might a rental property, check with the county tax records to identify the owner. They may be unaware of the situation and welcome the notification to protect their investment.

Another alternative might be to notify the homeowner’s association, if there is one. One of the benefits of a HOA is to enforce community appearance standards as set in the covenants or bylaws that specify how properties must be maintained. This could be a less personal method of reaching a beneficial outcome.

If the source of the problem is a code or housing violation, the city may be the ultimate authority. Most cities have a separate code and neighborhood services division and some cities have 311 for non-emergency assistance.

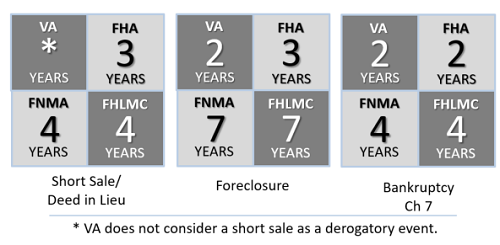

“How long do we have to wait to qualify for another mortgage” is the question concerning people who’ve had a foreclosure, short sale or bankruptcy.The loan types for the new loan will differ in amounts of time to heal credit scores based on the event.

The following chart is meant to be a general guide for how long a person might have to wait. During this waiting period, it’s important that the person be current on all payments and maintains a history of good credit.

A recommended lender can give you specific information regarding your individual situation and can make suggestions that will improve your ability to qualify for a mortgage. This process should be started before looking at homes because of the time constraints listed here can vary based on current requirements and possible extenuating circumstances of your case.

We want to be your personal source of real estate information and we’re committed to helping from purchase to sale and all the years in between. Call us at (225) 291-1234 for lender recommendations.

In the late 80’s, both FHA and VA began requiring buyers to qualify to assume their mortgages. The main reason there haven’t been many assumptions in the past 25 years is that interest rates have been steadily going down and if a person has to qualify, they might as well do it on a new loan and get a lower interest rate.

Based on projections by Fannie Mae, Freddie Mac, the MBA and NAR, rates for the second half of 2017 and 2018 are expected to be higher. When interest rates on new mortgages are higher than the rates of assumable FHA and VA mortgages in the recent past, it becomes more advantageous to assume the existing mortgages.

FHA and VA loans originated with lower than current interest rates have great advantages for buyers and sellers.

Interest rate won’t change for the qualified buyer

Lower interest rate means lower payments

Lower closing costs than originating a new mortgage

Easier to qualify for an assumption than a new loan

Lower interest rate loans amortize faster than higher ones

Equity grows faster because loan is further along the amortization schedule

Assumable mortgage could make the home more marketable

An Assumption Comparison can help determine the savings and financial benefits of an assumable mortgage with a lower rate.

An estate plan is a collection of documents to ensure that your wishes are carried out because of death or incapacity to make decisions for yourself. Spouses, minor children, adult children, property and investments can all be factors that should motivate a person to undergo the process.

Will – this document specifies the way a person wants to manage and distribute his/her assets after their death. When a person dies without a will, the laws of the state where the person resided will determine the distribution of the property.

Durable Power of Attorney – this document grants to a designated person the authority to act on behalf of the principal in in legal affairs should the principal become incapacitated. Among other things, this would allow the attorney-in-fact to buy and sell property on the behalf of the principal.

Healthcare Proxy – this document grants that a designated person can legally make healthcare decisions on behalf of the principal when they are incapable of making and executing specific decisions stated in the proxy.

Living Will – this document directs physicians with respect to life-prolonging medical treatments in case they become unable to communicate their decisions.

Hippa Release – this document allows heath care providers to release your health care information to a designated person. Otherwise, they are required by federal law to protect the privacy of your health information.

Letter of Instruction – This document contains information and instructions about a person’s wishes upon death. It is intended to offer details on whom to contact and where to find important documents about personal and financial matters.

Requirements of these documents can vary from state to state and legal advice should be obtained. If you need a current estimate of value on real estate that may be involved, usually a price opinion from a licensed real estate professional will suffice. It would be my privilege to assist you with this at no cost or obligation.

People who experience a property loss are usually asked by their insurance company for proof of purchase which can come in the form of a receipt or current inventory of their personal belongings.

Even the most organized people might find it challenging to find receipts for all the valuables in their home. If the inventory isn’t up-to-date, a homeowner might forget to add some items to the claim and may not recognize the omission for long after the claim is settled.

The inventory can serve as a guide to make sure a homeowner gets compensated for all the loss.

Photographs and videos can be adequate proof that the items belonged to the insured. A series of pictures of the different rooms, closets, cabinets and drawers are helpful. When video is used, consider commenting as it is shot and be sure to go slow enough and close enough to things becoming recorded.

For your convenience, download a Home Inventory, complete it, and save a copy off premise. Good places for your inventory could be a safety deposit box or digitally, in the cloud if you have server-based storage available like Dropbox.

With all the attention on Washington and what is going on at the White House, I thought it might be interesting to give a Real Estate angle to the situation. What do you think?