When deciding whether you should rent or buy, make sure you’re considering these factors.

Buying a home means consistent monthly payments. Homeownership also helps to build your wealth. And owning a home gives you greater flexibility than renting.

If you’re ready to take advantage of the perks of homeownership, let’s connect to explore your options.

Is a 20% Down Payment Really Necessary To Purchase a Home?

There’s a common misconception that, as a homebuyer, you need to come up with 20% of the total sale price for your down payment. In fact, a recent survey by Lending Tree asks what is keeping consumers from purchasing a home. For over half of those surveyed, the ability to afford a down payment is the biggest hurdle.

That may be because those individuals assume a 20% down payment is necessary. While putting more money down if you’re able can benefit buyers, putting 20% down is not mandatory. As Freddie Mac puts it:

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

If saving that much money sounds overwhelming, you might be ready to give up on the dream of homeownership before you even begin – but you don’t have to. According to the Profile of Home Buyers and Sellers from the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. It may sound surprising, but today’s average down payment is only 12%. That number is even lower for first-time homebuyers, whose average down payment is only 7%.

Based on the Home Buyers and Sellers Generational Trends Report from NAR, the graph below shows an even closer look at the down payment percentage various age groups pay:As the graph shows, the only groups who put 20% or more down on average are older homebuyers who likely can use the sale of an existing home to fuel a larger down payment on their next home.

What does this mean for you?

If you’re a prospective homebuyer, it’s important to know you don’t have to put the full 20% down. And while saving for any down payment amount may feel like a challenge, keep in mind there are programs for qualified buyers that allow them to purchase a home with a down payment as low as 3.5%. There are also options like VA loans and USDA loans with no down payment requirements for qualified applicants.

To understand your options, you do need to do your homework. If you’re interested in learning more about down payment assistance programs, information is available through sites like downpaymentresource.com. Be sure to also work with a real estate advisor from the start to learn what you may qualify for in the homebuying process.

Bottom Line

Don’t let the myth of the 20% down payment halt your homebuying process before it begins. If you want to purchase a home this year, let’s connect to start the conversation and explore your options.

When it comes to the current housing market, there are multiple misconceptions – from what the current supply of available homes looks like to how much houses are selling for.

It takes professionals who study expert opinions and data to truly understand the real estate market and separate fact from fiction.

Trust the pros. If you want to understand why it’s still a good time to buy, let’s connect today.

Home Price Appreciation Is Skyrocketing in 2021. What About 2022?

One of the major story lines over the last year is how well the residential real estate market performed. One key metric in the spotlight is home price appreciation. According to the latest indices, home prices are skyrocketing this year.

Here are the latest percentages showing the year-over-year increase in home price appreciation:

The dramatic increases are seen at every price point and in all regions of the country.

Increases Are Across Every Price Point

According to the latest Home Price Index from CoreLogic, each price range is seeing at least a 19% increase year-over-year:

Increases Are Across Every Region in the Country

Every region in the country is experiencing at least a 14.9% increase in home price appreciation, according to the Federal Housing Finance Agency (FHFA):

Increases Are Across Each of the Top 20 Metros in the Country

According to the U.S. National Home Price Index from S&P Case-Shiller, every major metro is seeing at least a 13.3% growth in prices (see graph below):

What About Price Appreciation in 2022?

Prices are the result of the balance between supply and demand. The demand for single-family homes has been strong over the last 18 months. The supply of houses available for sale was near historic lows. However, there’s some good news on the supply side. Realtor.comreports:

“432,000 new listings hit the national housing market in August, an increase of 18,000 over last year.”

There will, however, still be a shortage of supply compared to demand in 2022. CoreLogicreveals:

“Given the widespread demand and considering the number of standalone homes built during the past decade, the single-family market is estimated to be undersupplied by 4.35 million units by 2022.”

Yet, most forecasts call for home price appreciation to moderate in 2022. The Home Price Expectation Survey, a survey of over 100 economists, investment strategists, and housing market analysts, calls for a 5.12% appreciation level next year. Here are the 2022 home appreciation forecasts from the four other major entities:

Price appreciation is expected to slow in 2022 when compared to the record highs of 2021. However, it is still expected to be greater than the annual average of 4.1% over the last 25 years.

Bottom Line

If you owned a home over the past year, you’ve seen your household wealth grow substantially, and you’ll see another nice boost in 2022. If you’re thinking of buying, consider buying now as prices are forecast to continue increasing through at least next year.

In today’s real estate market, low inventory and high demand are driving up home prices. As many as 54% of homes are getting offers over the listing price, based on the latest Realtors Confidence Index from the National Association of Realtors (NAR). Shawn Telford, Chief Appraiser at CoreLogic, elaborates:

An economist responded when asked how interest rates would change: “They may fall some and then, rise and after that, they’ll fluctuate.”

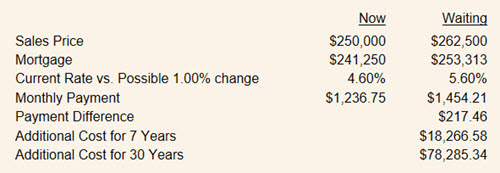

Just because interest rates have been low for ten years doesn’t mean they are supposed to be low. The Federal Reserve has raised interest rates twice this year and are expected to go up twice more plus three times next year. Mortgage rates have risen from 3.95% to 4.62% since the first of January.

Increased rates directly affect the payments on homes but so does the price. With inventory levels remaining low, the prices will continue to go up. When interest rates and prices rise at the same time, it costs buyers a lot more.

If the mortgage rates go up by one percent and prices increase by five percent in the next year, the payment on a $250,000 home could go up by $200 a month. In a seven-year period, the buyer would pay $18,000 more for the home.

People planning to buy a home, need to investigate the possibilities of accelerating their timetable to take advantage of lower rates and prices. Use the Cost of Waiting to Buy calculator to see how much more it could cost you to wait. Call Profile.BusinessPhone} if you have questions about what can be done now.

A home that isn’t being maintained like others in the neighborhood can negatively affect your visual sense of appeal and in some extreme cases, even affect property values. It might be an overgrown yard, a fence in need of repair, excessive noise, unruly pets, paint peeling on the home or even a car or boat parked in front of the home that hasn’t moved in weeks.

Most people want to be good neighbors and may be willing to correct an issue once it is brought to their attention. A practical but possibly, confrontational solution is to contact the responsible person and describe your perception of the issue. However, they may not always agree with the same urgency and it might be necessary to seek other remedies.

An owner-occupant may be more sympathetic to the neighbors and willing to correct the issue. If you think the home might a rental property, check with the county tax records to identify the owner. They may be unaware of the situation and welcome the notification to protect their investment.

Another alternative might be to notify the homeowner’s association, if there is one. One of the benefits of a HOA is to enforce community appearance standards as set in the covenants or bylaws that specify how properties must be maintained. This could be a less personal method of reaching a beneficial outcome.

If the source of the problem is a code or housing violation, the city may be the ultimate authority. Most cities have a separate code and neighborhood services division and some cities have 311 for non-emergency assistance.

Buyers who have been concerned about what might happen to the tax laws affecting home ownership should feel more comfortable about moving forward with their decision to purchase. The 2017 Tax Cut and Jobs Act passed by Congress and signed by the President continues to treat real estate as a favored investment.

Whether it is for a home to live in as your principal residence or to use as rental property, the tax laws are in place but other dynamics to be concerned with are not; mortgage rates are expected to rise as well as prices.

Reasons to buy now:

The mortgage interest deduction is intact for most taxpayers.

The capital gain exclusion for principal residences up to $500,000 remains in place.

Taxpayers can elect annually to take newly increased standard deduction or itemize deductions whichever will benefit them the most.

The house payment with taxes and insurance is most likely cheaper than the rent.

Rents will continue to rise making the difference even greater in the future.

Lock-in the principal & interest payment with a fixed-rate mortgage.

30-year mortgage terms are available to most borrowers.

Prices will likely increase due to lower inventories and several years of low housing starts.

Section 1031 exchanges, capital gains and depreciation remain the same for rental properties.

For a summary of specific real estate provisions in the 2017 Tax Cut and Jobs Act, click here.

It’s not “if” the rate goes up but “when” the rate goes up; it could make a big difference for some buyers. Freddie Mac predicts that mortgage rates will be at 4.5% a year from now.

If buyers can afford a home with higher interest rates, it means higher payments. Higher payments might mean they won’t have the money to spend on other things like furniture or improvements to the home or an unrelated purchase like a new car.

When the rate moves 0.50% on a $250,000, the payment goes up by $70.66 a month. If it moves 1.00%, the payment goes up by $143.74 per month, each and every month for the entire term of the mortgage which means paying over $50,000 more for the house.

The question facing every borrower in this situation is “How will you feel about having to pay more to live in the same house because you were not ready to commit?”

Then, there’s the borrower who is absolutely maxed out as to what they can qualify for or sometimes, it is a borrower who just refuses to pay a higher payment. When that’s the case, the buyer has to make a larger down payment. In the same example, a 0.50% increase in rate would require $14,873 more in down payment. That could make the purchase impossible or require the buyer to buy a lesser price home that will not have the same amenities.

Mortgage rates have been low for so long that some people think that is what they should be. There are some economists who believe that the economy will not be strong again until mortgage rates are in the 7% range.

Rental homes can be a natural alternative investment choice for homeowners because they are already familiar with houses. Maintenance on a rental is not that much different than on your personal home. The same plumbers, painters and other workmen can be used to make repairs.

Single family homes offer an investor high loan-to-value mortgages at fixed interest rates for long terms on appreciating assets with defined tax advantages and more control than other investments.

High loan-to-value mortgages – most investments require that you pay cash but rental properties can be purchased with 20% down payment.

Fixed interest rates – most commercial loans are based on a floating rate such as prime interest plus one or two percent compared to real estate loans as fixed rates for the term.

Long terms – commercial loans are generally short-term such as six months or a year with the possibility of being renewed for another six months or a year unlike real estate where a 30-year mortgage is commonplace.

Appreciating assets – real estate has a long-term history of going up in value.

Defined tax advantages – many investments are taxed as ordinary income but rental real estate enjoys a non-cash deduction called cost recovery, the profits from sale are taxed at lower long-term capital gains rates or may be eligible for a tax-deferred exchange.

Control – rental homes don’t require partners and afford the investor more options than investing in mutual funds and other traditional investments.

The demand for good rentals is strong and the rents continue to go up in most markets. There are people who choose not to buy or cannot buy a home who would prefer to live in a single family home rather than an apartment.

![Reasons Renters Buy [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/10/30142601/20211001-MEMa-1046x1991.png)

![Fact or Fiction: Homebuyer Edition [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/09/09142043/20210910-MEM-1046x1998.png)