For buyers, expect competition, be ready to move fast, and be prepared to submit your strongest offer. For sellers, know your house will be the center of attention and that it’ll likely sell quickly and get multiple offers.

If you’re ready to move, let’s connect to talk about our local area and how you can take advantage of today’s unprecedented housing market.

In today’s housing market, there are far more buyers looking for homes than sellers listing their houses. Based on the concept of supply and demand, this means home prices will naturally rise. Why is that? When there are more people trying to buy an item than there are making that item available for sale, that drives prices up. And that’s exactly the case in today’s housing market. So, knowing what’s happening with the inventory of homes for sale and the demand for housing is crucial for today’s buyers and sellers.

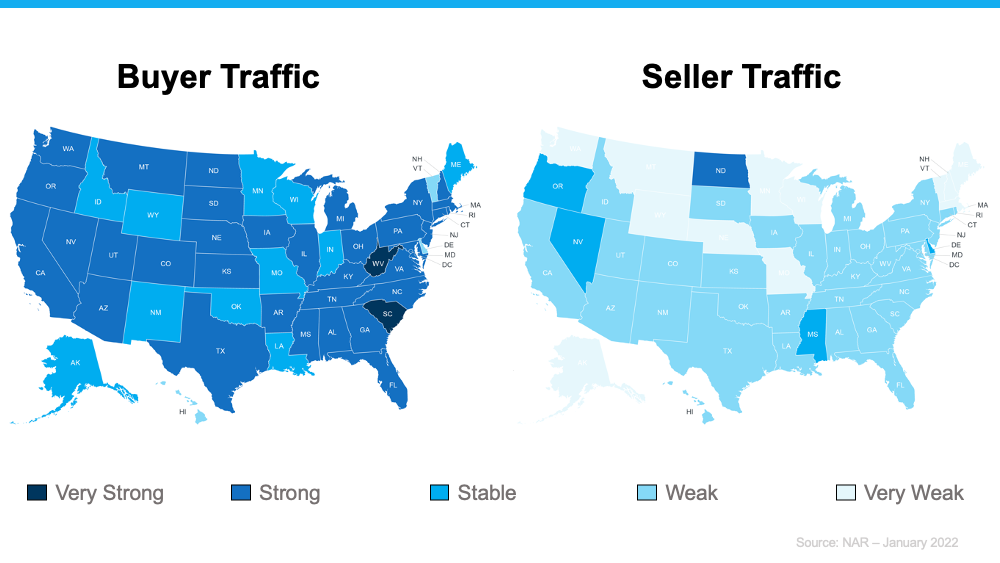

Nationally, Demand Is High and Supply Is Very Low

The latest buyer and seller activity data from the National Association of Realtors (NAR) indicates buyer traffic heavily outweighs seller traffic today, as shown in the maps below. There are far darker blues (strong buyer activity) on the left and much lighter blues (weak seller activity) on the right. In other words, this shows how the demand for homes is significantly greater than what’s available to purchase.

What Does This Mean if You’re a Seller?

Supply is struggling to keep pace with demand. In fact, the inventory of homes for sale recently hit an all-time low. That gives you an incredible advantage when you sell your house. With so few listings, it’s likely more potential buyers will view your house – especially if you work with an agent to price it right. That means there’s a high chance you’ll receive multiple offers or buyers will enter a bidding war for your house. And that dynamic can drive the sale price of your home up.

What Does This Mean if You’re a Buyer?

As a buyer with fewer options available, you’re likely to see more competition, so you need to be strategic to win. First, make sure you have a trusted professional on your side. Your real estate agent will help you understand your local market and work with you to act quickly when the time is right. Even when it’s challenging to find a home, you can still succeed as a buyer today if you have a trusted advisor on your side every step of the way.

Bottom Line

Whether you’re a homebuyer, seller, or both, knowledge truly is power. Let’s connect today so you can better understand what’s happening in our local market and achieve your homebuying and selling goals this year.

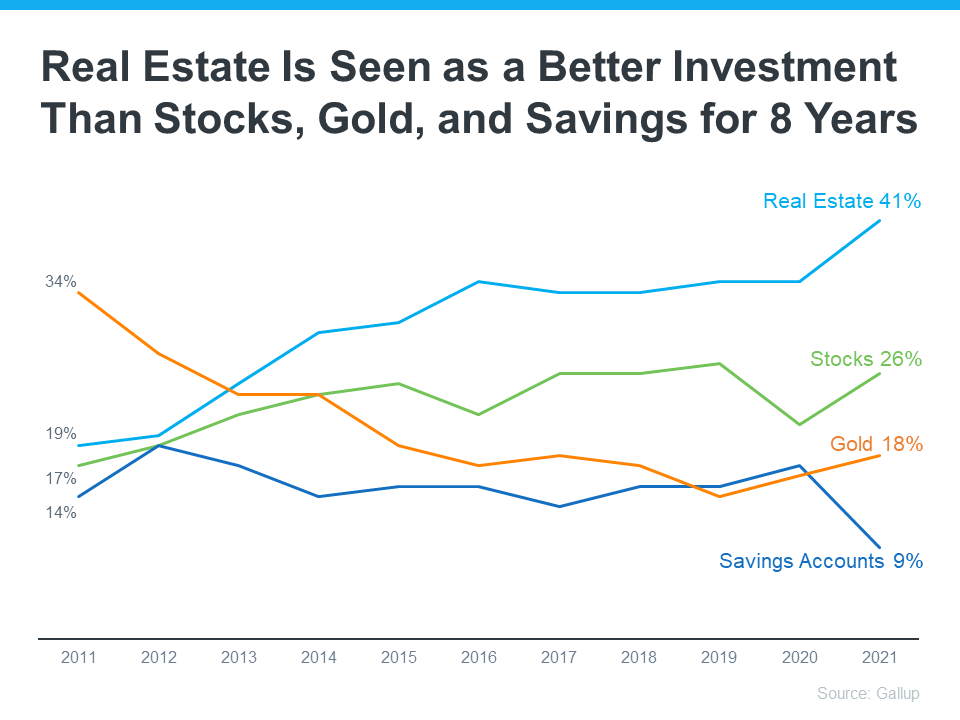

In an annual Gallup poll, Americans chose real estate as the best long-term investment. And it’s not the first time it’s topped the list, either. Real estate has been on a winning streak for the past eight years, consistently gaining traction as the best long-term investment (see graph below):

If you’re thinking about purchasing a home this year, this poll should reassure you. Even when inflation is rising like it is today, Americans agree an investment like real estate truly shines.

Why Is Real Estate a Great Investment During Times of

High Inflation?

With inflation reaching its highest level in 40 years, it’s more important than ever to understand the financial benefits of homeownership. Rising inflation means prices are increasing across the board. That includes goods, services, housing costs, and more. But when you purchase your home, you lock in your monthly housing payments, effectively shielding yourself from increasing housing payments. James Royal, Senior Wealth Management Reporter at Bankrate, explains it like this:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

If you’re a renter, you don’t have that same benefit, and you aren’t protected from increases in your housing costs, especially rising rents.

History Shows During Inflationary Periods, Home Prices

Rise as Well

As a homeowner, your house is an asset that typically increases in value over time, even during inflation. That‘s because, as prices rise, the value of your home does, too. And that makes buying a home a great hedge during periods of high inflation. Natalie Campisi, Advisor Staff for Forbes, notes:

“Tangible assets like real estate get more valuable over time, which makes buying a home a good way to spend your money during inflationary times.”

Bottom Line

Housing truly is a strong investment, especially when inflation is high. When you lock in a mortgage payment, you’re shielded from housing cost increases, and you own an asset that typically gains value with time. If you want to better understand how buying a home could be a great investment for you, let’s connect today.

When you’re selling any item, you usually want to sell it for the greatest profit possible. That happens when there’s a strong demand and a limited supply for that item. In the real estate market, that time is right now. If you’re thinking of selling your house this year, here are two reasons why now’s the time to list.

“Spring, the hottest time of year for homebuyers and sellers, has started early, according to economists. . . . ‘Home shopping season appears to already be in full swing!’”

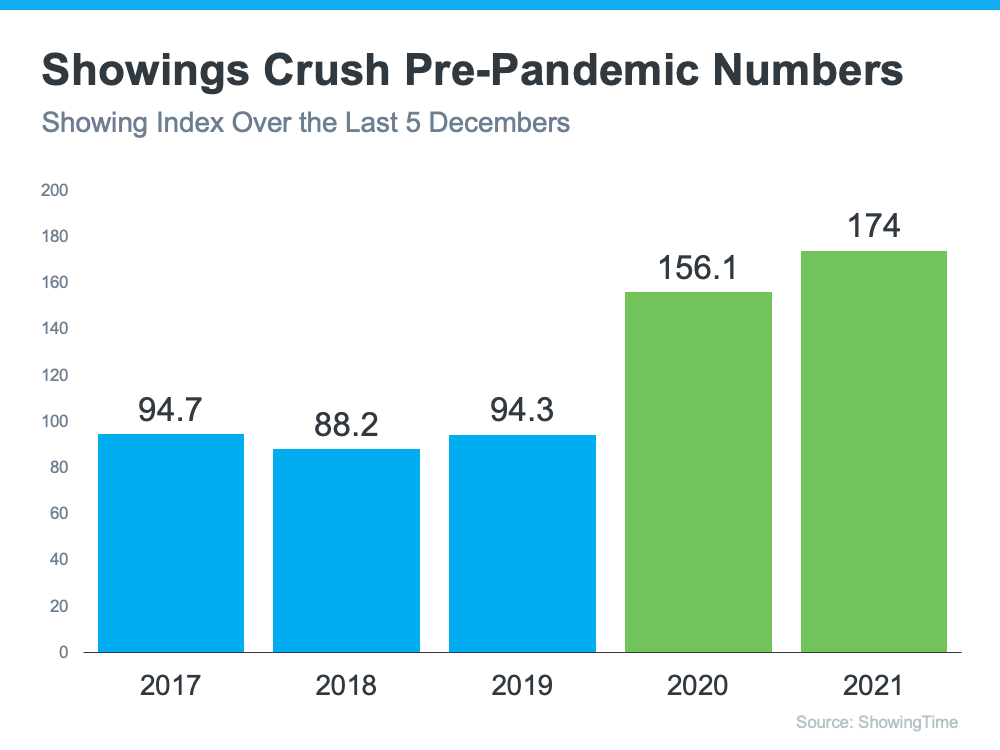

And they aren’t the only ones saying buyers are already out in full force. That claim is backed up with data released last week by ShowingTime. The ShowingTime Showing Index tracks the average number of monthly buyer showings on active residential properties, which is a highly reliable leading indicator of current and future trends for buyer demand. The latest index reveals this December was the most active December in five years (see graph below):

As the data indicates, buyers are very active this winter. Last December saw even more showings than December of 2020, which was already a stronger-than-usual winter. And remember – you want to sell something when there’s a strong demand for that item. That time is now.

2. Housing Supply Is Extremely Low

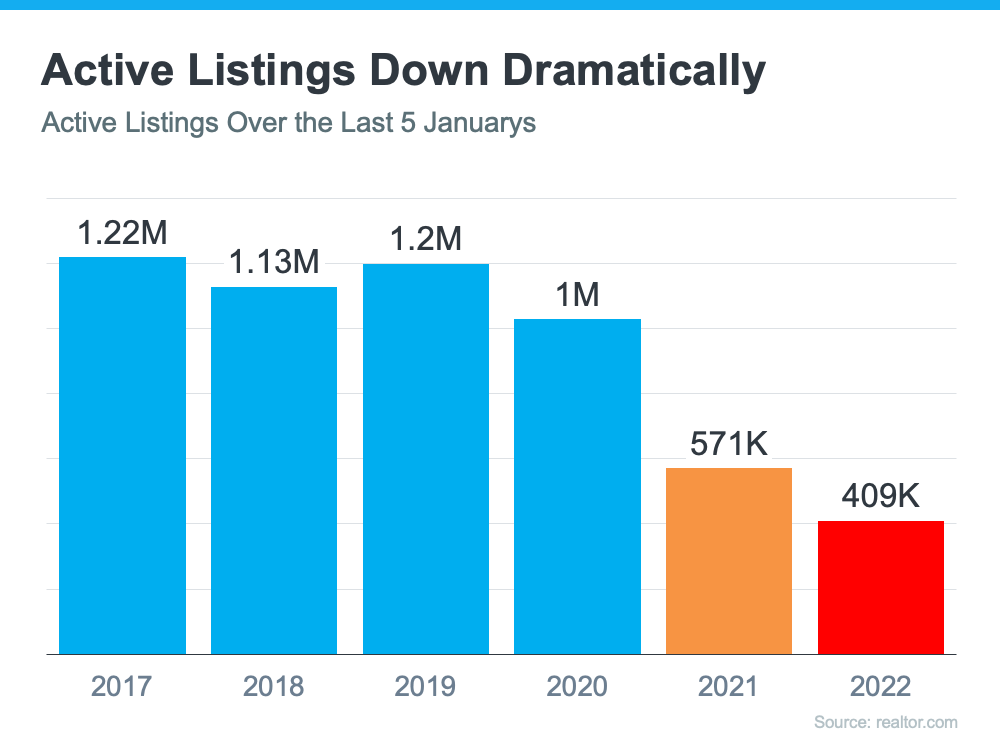

Each month, realtor.com releases data on the number of active residential real estate listings (listings currently for sale). Their most recent report reveals the latest monthly number is the lowest we’ve seen in any January since 2017 (see graph below):

And don’t forget, the best time to sell an item is when there’s a limited supply of it available. This graph clearly shows how extremely low housing supply is today.

Even Though Supply Is at a Historic Low, Home Sales Are

at a 15-Year High

According to the latest Existing Home Sales Report from the National Association of Realtors (NAR), existing-home sales totaled 6.12 million in 2021 – the highest annual level since 2006. This means the market is hot and homeowners are in a great place to sell now while sales are so strong.

NAR also reports available listings by calculating the current months’ supply of inventory. They explain:

“Months’ supply refers to the number of months it would take for the current inventory of homes on the market to sell given the current sales pace.”

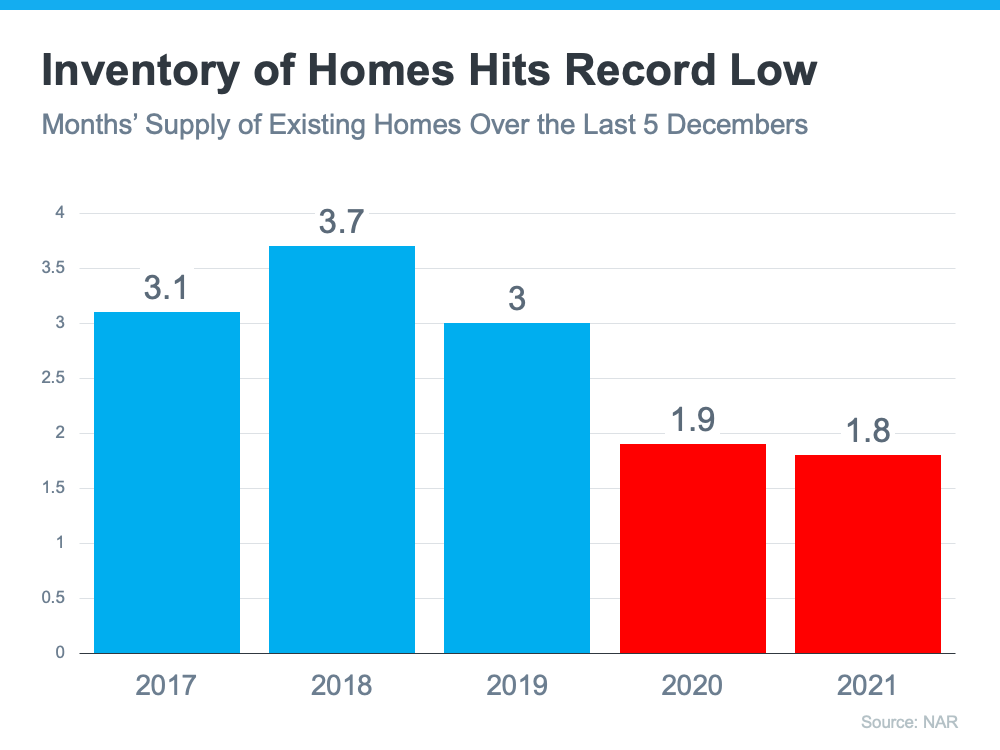

The current 1.8-months’ supply is the lowest ever reported. Here are the December numbers over the last five years (see graph below):

The ratio of buyers to sellers favors homeowners right now to a greater degree than at any other time in history. Buyer demand is high, and supply is low. That gives sellers like you an incredible opportunity.

Bottom Line

If you agree the best time to sell anything is when demand is high and supply is low, let’s connect to begin discussing the process of listing your house today.

If you were thinking about buying a home this year, but already pressed pause on your plans due to rising home prices and increasing mortgage rates, there’s something you should consider. According to the latest report from ATTOM Data, owning a home is more affordable than renting in the majority of the country. The 2022 Rental Affordability Report says:

“. . . Owning a median-priced home is more affordable than the average renton a three-bedroom property in 666, or 58 percent, of the 1,154 U.S. counties analyzed for the report. That means major home ownership expenses consume a smaller portion of average local wages than renting.”

Other experts in the industry offer additional perspectives on renting today. In the latest Single-Family Rent Index from CoreLogic, single-family rent saw the fastest year-over-year growth in over 16 years when comparing data for November each year (see graph below):

Molly Boesel, Principal Economist at CoreLogic, stresses the importance of what the data shows:

“Single-family rent growth hit its sixth consecutive record high. . . . Annual rent growth . . . was more than three times that of a year earlier. Rent growth should continue to be robust in the near term, especially as the labor market continues to improve.”

What Does This Mean for You?

While it’s true home prices and mortgage rates are rising, so are monthly rents. As a prospective buyer, rising rates and prices shouldn’t be enough to keep you on the sideline, though. As the chart above shows, rents are skyrocketing. The big difference is, when you rent, that rising cost benefits your landlord’s investment strategy, but it doesn’t deliver any sort of return for you.

In contrast, when you buy a home, your monthly mortgage payment serves as a form of forced savings. Over time, as you pay down your loan and as home values rise, you’re building equity (and by extension, your own net worth). Not to mention, you’ll lock in your mortgage payment for the duration of your loan (typically 15 to 30 years) and give yourself a stable and reliable monthly payment.

When asking yourself if you should keep renting or if it’s time to buy, think about what Todd Teta, Chief Product Officer at ATTOM Data, says:

“. . . Home ownership still remains the more affordable option for average workers in a majority of the country because it still takes up a smaller portion of their pay.”

If buying takes up a smaller portion of your pay and has benefits renting can’t provide, the question really becomes: is renting really worth it?

Bottom Line

If you’re weighing your options between renting and buying, it’s important to look at the full picture. While buying a home can feel like a daunting process, having a trusted advisor on your side is key. Let’s connect to explore your options so you can learn more about the benefits of homeownership today.

If you’re thinking about selling your house in 2022, you truly have a once-in-a-lifetime opportunity at your fingertips. When selling anything, you always hope for strong demand for the item coupled with a limited supply. That maximizes your leverage when you’re negotiating the sale. Home sellers are in that exact situation right now. Here’s why.

Demand Is Very Strong

According to the latest Existing Home Sales Report from the National Association of Realtors (NAR), 6.18 million homes were sold in 2021. This was the largest number of home sales in 15 years. Lawrence Yun, Chief Economist for NAR, explains:

“Sales for the entire year finished strong, reaching the highest annual level since 2006. . . . With mortgage rates expected to rise in 2022, it’s likely that a portion of December buyers were intent on avoiding the inevitable rate increases.”

Demand isn’t expected to weaken this year, either. In addition, the Mortgage Finance Forecast, published last week by the Mortgage Bankers’ Association (MBA), calls for existing-home sales to reach 6.4 million homes this year.

Supply Is Very Limited

The same sales report from NAR also reveals the months’ supply of inventory just hit the lowest number of the century. It notes:

“Total housing inventory at the end of December amounted to 910,000 units, down 18% from November and down 14.2% from one year ago (1.06 million). Unsold inventory sits at a 1.8-month supply at the present sales pace, down from 2.1 months in November and from 1.9 months in December 2020.”

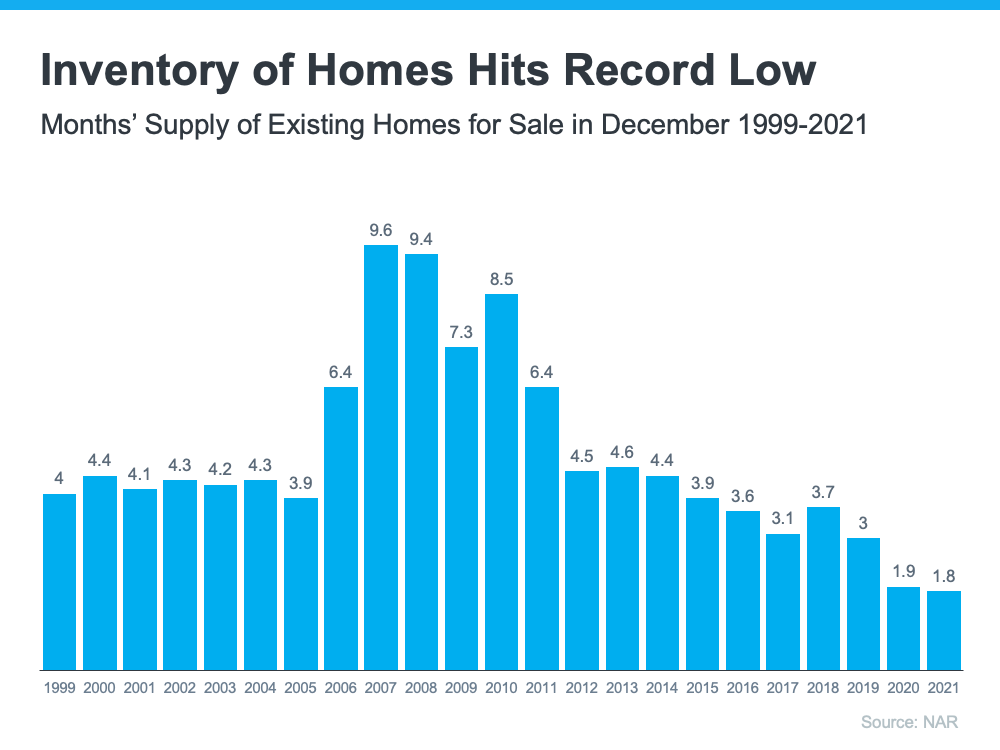

The reality is, inventory decreases every year in December. That’s just how the typical seasonal trend goes in real estate. However, the following graph emphasizes how this December was lower than any other December going all the way back to 1999.

Right Now, Sellers Have Maximum Leverage

As mentioned above, when there’s strong demand for an item and a limited supply of it available, the seller has maximum leverage in the negotiation. In the case of homeowners who are thinking about selling, there may never be a better time than right now. While demand is this high and inventory is this low, you’ll have leverage in all aspects of the sale of your house.

Today’s buyers know they need to be flexible negotiators that make very competitive offers, so here are a few areas that could tip in your favor when your house goes on the market:

Competitive sales price

Flexible closing date

Potential for a leaseback to allow you more time to find a home

Minimal offer contingencies

Bottom Line

If you’re thinking of selling your house this year, now is the optimal time to list it. Let’s connect to discuss how you can put your house on the market today.

Last week, the average 30-year fixed mortgage rate from Freddie Macjumped from 3.22% to 3.45%. That’s the highest point it’s been in almost two years. If you’re thinking about buying a home, this news may have come as a bit of a shock. But the truth is, it wasn’t entirely unexpected. Experts have been calling for rates to rise in their 2022 projections, and the forecast is now becoming a reality. Here’s a look at the projections from Freddie Mac for this year:

Q1 2022: 3.4%

Q2 2022: 3.5%

Q3 2022: 3.6%

Q4 2022: 3.7%

As the numbers show, this jump in rates is in line with the expectations from Freddie Mac. And what they also indicate is that mortgage rates are projected to continue climbing throughout the year. But should you be worried about rising mortgage rates? What does that really mean for you?

As rates increase even modestly, they impact your monthly mortgage payment and overall affordability. If you’re looking to buy a home, rising mortgage rates should be an incentive to act sooner rather than later.

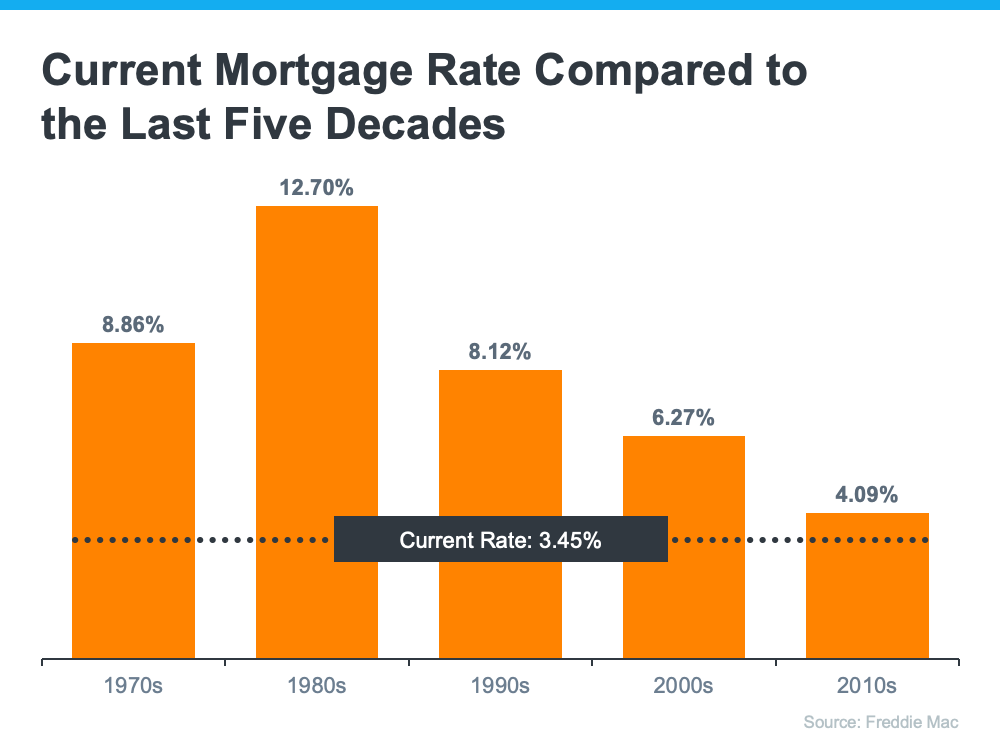

The good news is, even though rates are climbing, they’re still worth taking advantage of. Historical data shows that today’s rate, even at 3.45%, is still well below the average for each of the last five decades (see chart below):

That means you still have a great opportunity to buy now with a rate that’s better than what your loved ones may have paid in decades past. If you buy a home while rates are in the mid-3s, your monthly mortgage payment will be locked in at that rate for the life of your loan. As you can see from the chart above, a lot can change in that time frame. Buying now is a great way to protect yourself from rising costs and future rate increases while also securing your payment amount for the long term.

Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), says:

“Mortgage rates surged in the second week of the new year. The 30-year fixed mortgage rate rose to 3.45% from 3.22% the previous week. If inflation continues to grow at the current pace, rates will move up even faster in the following months.”

Bottom Line

Mortgage rates are increasing, and they’re forecast to be even higher by the end of 2022. If you’re planning to buy this year, acting soon may be your most affordable option. Let’s connect to start the homebuying process today.

Many homeowners who plan to sell in 2022 may think the wise thing to do is to wait for the spring buying market since historically about 40 percent of home sales occur between April and July. However, this year’s expected to be much different than the norm. Here are five reasons to list your house now rather than waiting until the spring.

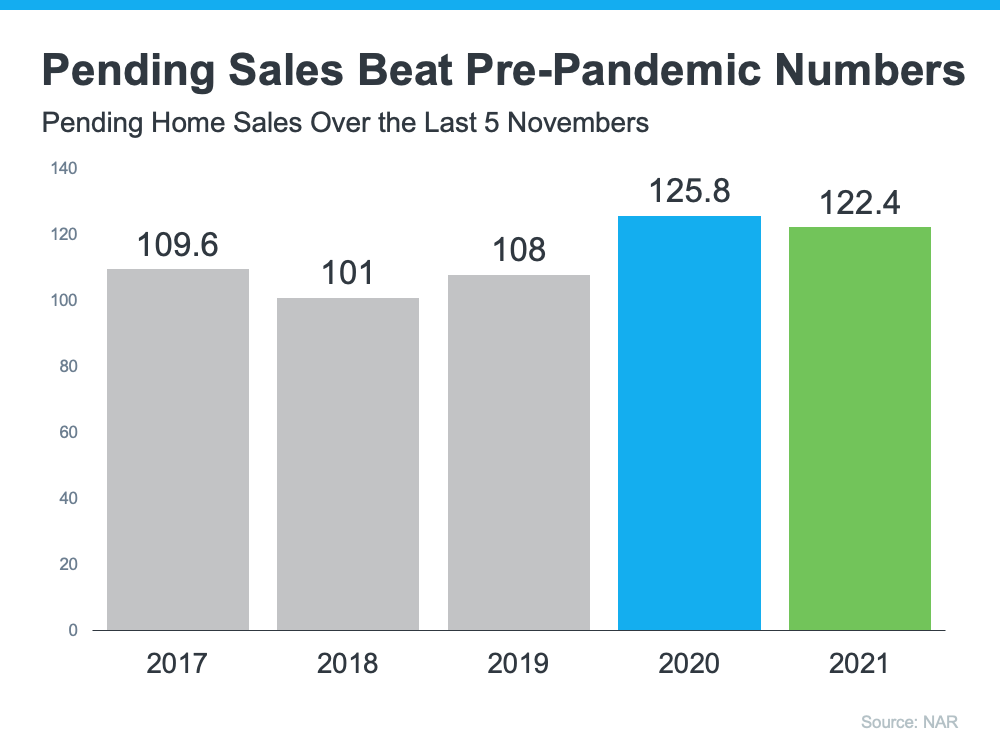

1. Buyers Are Looking Right Now, and They’re Ready To

Purchase

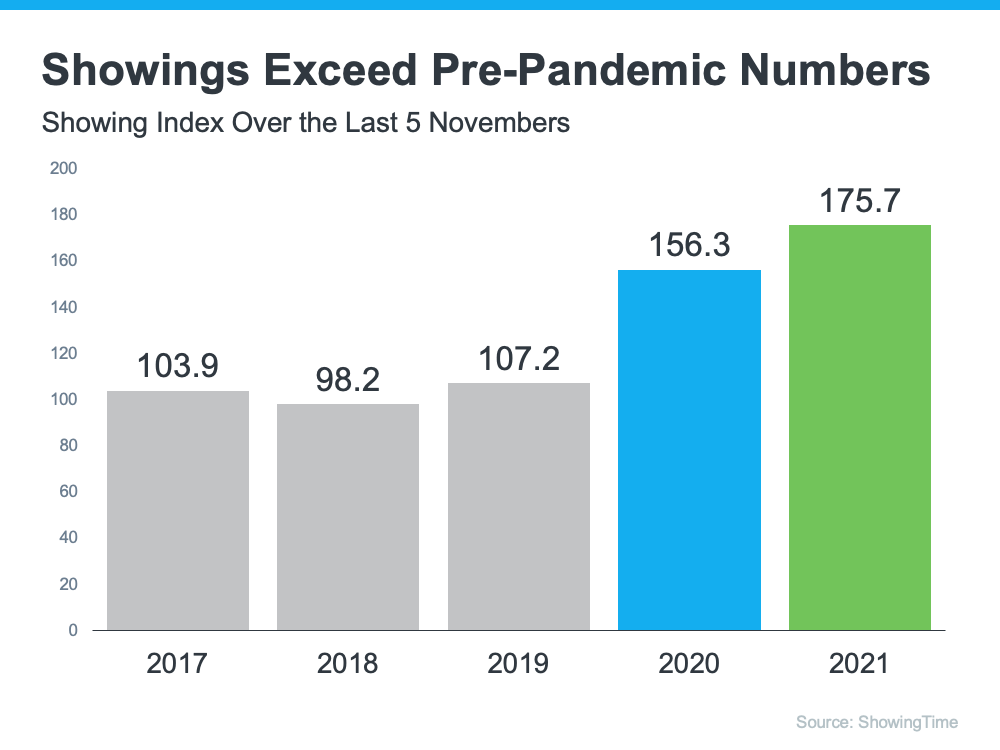

The ShowingTime Showing Index reports data from more than six million property showings scheduled across the country each month. In other words, it’s a gauge of how many buyers are out looking at homes at the current time.

The latest index, which covers November showings, reveals that buyers are still very active in the market. Comparing this November’s numbers to previous years, this graph shows that the index is higher than last year and much higher than the three years prior to the pandemic. Clearly, there’s an influx of buyers searching for your home.

Also, at this time of year, only those purchasers who are serious about buying a home will be in the market. You and your loved ones won’t be inconvenienced by casual searchers. Freddie Mac addresses this in a recent blog:

“The buyers who are willing to house hunt in a winter market, when there are fewer options, are typically more serious. Plus, year-end bonuses and overtime payouts give people more purchasing power.”

And that theory is proving to be true right now based on the number of buyers who have put a home under contract to purchase. The National Association of Realtors (NAR) publishes a monthly Pending Home Sales Index which measures housing contract activity. It’s based on signed real estate contracts for existing single-family homes, condos, and co-ops. The latest index shows:

“…housing demand continues to be high. . . . Homes placed on the market for sale go from ‘listed status’ to ‘under contract’ in approximately 18 days.”

Comparing the index to previous Novembers, while it’s slightly below November 2020 (when sales were pushed to later in the year because of the pandemic), it’s well above the previous three years.

The takeaway for you: There are purchasers in the market, and they’re ready and willing to buy.

2. Other Sellers Plan To List Earlier This Year

The law of supply and demand tells us that if you want the best price possible and to negotiate your ideal contract terms, put your house on the market when there’s strong demand and less competition.

A recent study by realtor.com reveals that, unlike in previous years, sellers plan to list their homes this winter instead of waiting until spring or summer. The study shows that 65% of sellers who plan to sell in 2022 have either already listed their home (19%) or are planning to put it on the market this winter.

Again, if you’re looking for the best price and the ability to best negotiate the other terms of the sale of your house, listing before this competition hits the market makes sense.

3. Newly Constructed Homes Will Be Your Competition in

the Spring

In 2020, there were over 979,000 new single-family housing units authorized by building permits. Many of those homes have yet to be built because of labor shortages and supply chain bottlenecks brought on by the pandemic. They will, however, be completed in 2022. That will create additional competition when you sell your house. Beating these newly constructed homes to the market is something you should consider to ensure your house gets as much attention from interested buyers as possible.

4. There Will Never Be a Better Time To Move-Up

If you’re moving into a larger, more expensive home, consider doing it now. Prices are projected to appreciate by approximately 5% over the next 12 months. That means it will cost you more (both in down payment and mortgage payment) if you wait. You can also lock in your 30-year housing expense with a mortgage rate in the low 3’s right now. If you’re thinking of selling in 2022, you may want to do it now instead of waiting, as mortgage rates are forecast to rise throughout the year.

5. It May Be Time for You To Make a Change

Consider why you’re thinking of selling in the first place and determine whether it’s worth waiting. Is waiting more important than being closer to your loved ones now? Is waiting more important than your health? Is waiting more important than having the space you truly need?

Only you know the answers to those questions. Take time to think about your goals and priorities as we move into 2022 and consider what’s most important to act on now.

Bottom Line

If you’ve been debating whether or not to sell your house and are curious about market conditions in your area, let’s connect so you have expert advice on the best time to put your house on the market.

As a buyer in a sellers’ market, sometimes it can feel like you’re stuck between a rock and a hard place. When you’re ready to make an offer on a home, remember these five easy tips to help you rise above the competition.

1. Know Your Budget

Knowing your budget and what you can afford is critical to your success as a homebuyer. The best way to understand your numbers is to work with a lender so you can get pre-approved for a loan. As Freddie Mac puts it:

“This pre-approval allows you to look for a home with greater confidence and demonstrates to the seller that you are a serious buyer.”

Showing sellers you’re serious can give you a competitive edge, and it helps you act quickly when you’ve found your perfect home.

2. Be Ready To Move Fast

Homes are selling quickly in today’s competitive housing market. According to the Existing Home Sales Reportfrom the National Association of Realtors (NAR):

“Eighty-three percent of homes sold in November 2021 were on the market for less than a month.”

When houses are selling this fast, staying on top of the market and moving quickly are key. Your agent can help you put together and submit your best offer as soon as you find the home you want to buy.

3. Lean on a Real Estate Professional

No matter what the housing market looks like, rely on a trusted real estate advisor. As Freddie Mac also notes:

“The success of your homebuying journey largely depends on the company you keep. . . . Be sure to select experienced, trusted professionals who will help you make informed decisions and avoid any pitfalls.”

Agents are experts in the local real estate market. They have insight into what’s worked for other buyers in your area and what sellers may be looking for in an offer. It may seem simple, but catering to what a seller needs can help your offer stand out.

4. Make a Strong, but Fair Offer

According to the latest Realtors Confidence Indexfrom NAR, 40% of offers today are above the list price. In such a competitive market, emotions and prices can run high. Having an agent to help you submit a strong, yet fair offer is critical in these situations. Your agent can help you understand the market value of the home and recent sales trends in the area.

5. Be a Flexible Negotiator

When putting together an offer, your trusted real estate advisor will help you consider which levers you can pull, including contract contingencies (conditions you set that the seller must meet for the purchase to be finalized). Of course, there are certain contingencies you don’t want to give up. Freddie Mac explains:

“Resist the temptation to waive the inspection contingency, especially in a hot market or if the home is being sold ‘as-is’, which means the seller won’t pay for repairs. Without an inspection contingency, you could be stuck with a contract on a house you can’t afford to fix.”

Bottom Line

Today’s competitive landscape makes it more important than ever to make a strong offer on a home. Let’s connect to make sure you rise to the top along the way.

Since the pandemic began, Americans have reevaluated the meaning of the word home. That’s led some renters to realize the many benefits of homeownership, including the feelings of security and stability and the financial benefits that come with rising home equity. At the same time, many current homeowners have decided their house no longer meets their needs, so they moved into homes with more space inside and out, including a home office for remote work.

However, not every purchaser has been able to fulfill their desire for a new home. Here are two obstacles some homebuyers are facing:

The ability to save for a down payment

The ability to qualify for a mortgage at the current lending standards

This past week, both of those challenges have been mitigated to some degree for many purchasers. The FHFA (which handles mortgages by Freddie Mac, Fannie Mae, and the Federal Housing Administration) is raising its loan limit for prospective purchasers in 2022. The term used to describe the maximum loan amount they will entertain is the Conforming Loan Limit.

What Is the Difference Between a Conforming Loan and a

Non-Conforming Loan?

Investopedia explains the difference in a recent post:

“Conforming loans are the only loans that meet the requirements to be acquired by Fannie Mae and Freddie Mac. Jumbo loans, which exceed the conforming limit, are the most common type of nonconforming loan.”

What Difference Does It Make to Me as a Home Buyer?

A Forbesarticle earlier this year explains the benefits of a conforming loan and why they exist:

“Since lenders can’t sell non-conforming loans to Fannie Mae or Freddie Mac to free up their cash, they’re a bit riskier for the lender. This is especially true for jumbo loans, which aren’t backed by any government guarantees. If you default on a jumbo loan, it’s a huge blow to the lender.

Thus, lenders generally charge higher interest rates to compensate, and they can have even more requirements. For example, lenders who give out jumbo loans often require that you make a down payment of at least 20% and show that you have at least six months’ worth of cash in reserve, if not more.”

What Happened Last Week?

The FHFA has significantly increased its Conforming Loan Limits for 2022. Sandra L. Thompson, FHFA Acting Director, explains in the press release that:

“Compared to previous years, the 2022 Conforming Loan Limits represent a significant increase due to the historic house price appreciation over the last year. While 95 percent of U.S. counties will be subject to the new baseline limit of $647,200, approximately 100 counties will have conforming loan limits approaching $1 million.”

This means that more homes now qualify for a conforming loan with lower down payment requirements and easier lending standards – the two challenges holding many buyers back over the last year.

The Federal Housing Administration (FHA) also increased its Conforming Loan Limits for 2022. That could also mean an easier path to homeownership for many prospective buyers. As the Forbes article explains:

“FHA loans can be very beneficial if you don’t have as much savings, or if your credit score could use some work.”

Bottom Line

Buying your first or your next home may have just gotten much easier (less stringent qualifying standards) and less expensive (possibly lower mortgage rate). Let’s connect to discuss how these changes may impact you.

Resources:

To get more information on the new FHFA Conforming Loan Limits, click here.

To get more information on the new FHA Conforming Loan Limits, click here.

![Supply and Demand in Today’s Market [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/03/03164955/20220304-MEM-1046x2586.png)