Many potential home buyers give up before they’ve even gotten started because they think they don’t have enough for a down payment. Often times it’s because they’ve bought into the myth that you can’t buy a home with less than a 20% down payment. Use our free infographic to show potential buyers that their dream is within reach and that now is the time to start their search.

Email it to potential clients, post it on your website, or use it in a blog post. Here are some post ideas to get you started:

YOU CAN BOTHER TEAM SISTERS ANYTIME…. YOUR AGENTS FOR LIFE!

Real estate agents hear this all the time…

“I wish I had called you before. But I just didn’t want to bother you. I know you’re busy…”

…after it is too late.

There are times when you might feel like you shouldn’t “bother” the real estate agent you know. (Could be your friend, a neighbor, your brother-in-law, cousin, your sister…)

Maybe you’re truly trying to be considerate.

But, maybe it’s because you’re not even aware that you should.

Or, you just don’t want to feel obligated or pushed into doing something. (Despite what many people think, most agents are not pushy. Most are the exact opposite.)

So, let’s go over a few times that you should “bother” your real estate agent. Because it really isn’t a bother.

In fact, we’ll get into why it will bother them if you don’t reach out to them for any of these things.

1. You just want to check out a house.

You see a house online. Or a For Sale sign. Maybe even just stumble across an open house.

You’re not all that serious about buying a house. Maybe you’re only just starting to think about it. Or, maybe you have no desire at all to move, and you’re just curious and want to take a peek.

So, you don’t want to “bother” the agent you know to show you the house.

Instead, you call the listing agent. Or some random agent you don’t even know. Or just walk right into the open house.

Next thing you know, you love the house. You’re making an offer. The offer is accepted. And then you regret it. Or problems come up. Or the process is miserable. Or you don’t feel like the agent you’re dealing with is giving you the best advice.

And that’s when you call the agent you know.

Too late. At that point, the agent you know can’t help. (Or at least shouldn’t…) Because now you are represented by another agent. The agent you know can get in a lot of trouble for even giving you friendly advice.

As innocent as it seems, when you just want to go see a house… you are inadvertently making a bigger decision than you think — you are deciding who will represent your interests, advise you, and help you through the process.

Even if you just go see a house with another agent, and before you even make an offer you decide to have the agent you know write up the offer and represent you… the agent who simply showed you the house could claim you as their client. It’s called “procuring cause”. I won’t get into the details here, but it can become messy.

You’re better off calling the agent you know to show you the house in the first place. You won’t be considered a bother.

What will bother him is to have to bite his tongue and not give you the help you want further into the process.

2. You want to know how much your home is worth.

Maybe you’re just curious about how much your home is worth. Or, maybe you’re actually thinking of selling. It might be because you want to get a feel for your net worth.

Nowadays, you can hop online and check out any number of sites that will give you the value of your home.

So, why “bother” the agent you know about this?

Because most of what you will find online is highly inaccurate to begin with. They are “automated” valuations. They are based upon data and algorithms. They have never even seen the inside of your home. They do not take into account your local market conditions.

And if you base your hopes, dreams, and decisions off of an inaccurate value, that can hurt you quite a bit.

Again, asking the agent you know to do an analysis and give you a true market value… not a bother.

But, it would be bothersome to hear that you’ve based important life decisions off of an inaccurate value once it’s too late.

3. You are considering a home improvement project.

The real estate agent you know probably isn’t an architect. Or a builder, a plumber, an electrician, a painter, etc. So, they probably can’t advise you about the ins and outs of a specific project or costs.

But once you have a sense of the proposed cost of a project, before you just pull the trigger and move forward, you really should “bother” your agent for their input.

Putting on an addition? That will surely increase the value.

A kitchen or bathroom remodel? Yep, your house will be worth more.

But will the value increase more than the amount you spent? Will that matter in your situation? Will the choices you make in decor, layout, or fixtures appeal to a buyer down the road? Does that even matter, given your future plans?

All questions and thoughts your agent can get into with you. Before you spend the money and go through the headaches of a huge project.

On the other hand, if you go forward with a home improvement project and spend, let’s say $60,000, and then call your agent…

You could seriously regret how much you spent, or even doing the project at all.

Your agent doesn’t want to break the news to you that your home is only worth $38,000 more after you spent $60,000. There is no joy in that. There is nothing that can be done at that point.

That’s just three examples. There are certainly more. But you get the point…

So, reach out to your agent before you do anything real estate related… and just trust that it isn’t a “bother”.

It’s a New Year Coming.. So that means Goal Setting Time. Have you thought about what your focus will be in 2020? If you would like help with any thing relating to Home Ownership we are here to help you meet your goals this coming year.

Each fall, decorators begin to share the interior design trends we can expect to see in the new year. Looking ahead to 2019, bold colors, metallics, and statement ceilings take center stage.

If you’re planning to put your place on the market and want it to appear like the freshest spot on the block, you need to know what’s hot and what’s not.

There is much more than a lower rate and payment to determine whether to refinance a mortgage. Lenders try to make refinancing as attractive as possible by rolling the closing costs into the new mortgage so there isn’t any out of pocket cash required.

The closing costs associated with a new loan could add several thousand dollars to your mortgage balance. The following suggestions may help you to reduce the expense to refinance.

? Tell the lender up-front that you want to have the loan quoted with minimal closing costs.

? Check with your existing lender to see if the rate and closing costs might be cheaper.

? Shop around with other lenders and compare rate and closing costs.

? If you’re refinancing an FHA or VA loan, consider the streamline refinance.

? Credit unions may have lower closing costs because they are generally loaning deposits and their cost of funds is less.

? Reducing the loan-to-value so mortgage insurance is not required will reduce expenses and lower the payment.

? Ask if the lender can use an AVM, automated valuation model, instead of an appraisal.

? You may not need a new survey if no changes have been made.

? There may be a discount on the mortgagee’s title policy available on a refinance.

? Points on refinancing, unlike a purchase, are ratably deductible over the life of the loan ($3,000 in points on a 30-year loan would result in a $100 tax deduction each year.)

? Consider a 15-year loan. If you can afford the higher payments, you can expect a lower interest rate than a 30-year loan and obviously, it will build equity faster and pay off in half the time.

A lender must provide you a list of the fees involved with making the loan within 3 days of making a loan application in the form of aLoan Estimate and a Closing Disclosure Form. Every dollar counts, and they belong to you.

When comparing the cost of owning a home to renting, there is more than the difference in house payment against the rent currently being paid. It very well could be lower than the rent but when you consider the other benefits, owning could be much lower than renting.

Each mortgage payment has an amount that is used to pay down the principal which is building equity for the owner. Similarly, the home appreciates over time which also benefits the owner by increasing their equity.

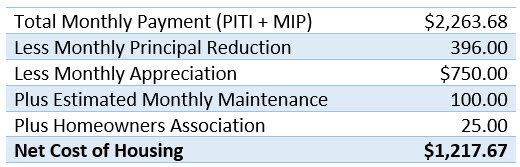

There are additional expenses for owning a home that renters don’t have like repairs and possibly, a homeowner’s association. To get a clear picture, look at the following example of a $300,000 home with a 3.5% down payment on a 4.5%, 30-year mortgage.

The total payment is $2,264 including principal, interest, property taxes, property and mortgage insurance. However, when you consider the monthly principal reduction, appreciation, maintenance and HOA, the net cost of housing is $1,218. It costs $1,282 more to rent at $2,500 a month than to own. In a year’s time, it would cost $15,000 more to rent than to own which is more than the down payment and closing costs to buy the home.

With normal amortization and 3% annual appreciation, the $10,500 down payment in this example turns into $112,00 in equity in seven years. Check out your own numbers using the Rent vs. Own or call me at (225) 291-1234. Owning a home makes sense and can be one of the best investments a person will ever make.

Acquisition Debt is the amount of money borrowed used to buy, build or improve a principal residence or second home. Under the new tax law, mortgages taken after 12/14/17 are limited to a combination of $750,000 on the first and second homes. The mortgage interest on this debt is tax deductible when itemizing deductions.

It is a dynamic number that is reduced with each payment as the unpaid balance goes down. The only way to increase acquisition debt is to borrow money to make capital improvements.

Prior to the new law, homeowners could additionally borrow up to $100,000 of home equity debt for any purpose and deduct the interest when itemizing deductions. Mortgage interest on home equity debt is no longer deductible unless it is for capital improvements.

Acquisition debt cannot be increased by refinancing. Some confusion occurs because mortgage lenders are concerned in making home loans that will be repaid according the terms of the note and using the home as collateral. That does not include making a tax-deductible mortgage.

Another thing that adds confusion to the issue is that the lenders will annually report how much interest was paid in a year but only the amount that is attributable to acquisition debt is deductible.

Even if the interest on the cash-out refinance is not deductible, it may be advantageous to pay off higher interest debt such as credit card debt and replacing it with lower mortgage debt.

It is the responsibility of the taxpayer to know what part of their mortgage debt is deductible. The challenge becomes more difficult after a cash-out refinance. Homeowners should keep records of all financing and capital improvements and consult with their tax professional.

It’s common for Sellers to consider offering a home warranty or protection plan to make their home more marketable. A growing number of homeowners are now purchasing this type of protection for themselves to limit the unexpected expenses of repairs and replacements.

A home protection plan is a renewable service contract that covers the repair or replacement of many of the components in a home. Some homeowners especially like the convenience that it organizes a qualified service provider as well as the cost of the repairs or replacements.

There are a variety of companies that offer home warranties and the coverage may differ but the majority of things will include heating, air conditioning, most built-in and some free-standing appliances, as well as other specific items. Additional specific coverage may be available for other items like pool and spa equipment.

Some investors are even placing this coverage on their rental properties to limit the amount of repairs during the year. It is a viable way to manage the financial risk and the stress dealing with unexpected expenses.

Call me at (225) 933-7062 if you’d like a recommendation of available programs.