When it comes to the current housing market, there are multiple misconceptions – from what the current supply of available homes looks like to how much houses are selling for.

It takes professionals who study expert opinions and data to truly understand the real estate market and separate fact from fiction.

Trust the pros. If you want to understand why it’s still a good time to buy, let’s connect today.

Home Price Appreciation Is Skyrocketing in 2021. What About 2022?

One of the major story lines over the last year is how well the residential real estate market performed. One key metric in the spotlight is home price appreciation. According to the latest indices, home prices are skyrocketing this year.

Here are the latest percentages showing the year-over-year increase in home price appreciation:

The dramatic increases are seen at every price point and in all regions of the country.

Increases Are Across Every Price Point

According to the latest Home Price Index from CoreLogic, each price range is seeing at least a 19% increase year-over-year:

Increases Are Across Every Region in the Country

Every region in the country is experiencing at least a 14.9% increase in home price appreciation, according to the Federal Housing Finance Agency (FHFA):

Increases Are Across Each of the Top 20 Metros in the Country

According to the U.S. National Home Price Index from S&P Case-Shiller, every major metro is seeing at least a 13.3% growth in prices (see graph below):

What About Price Appreciation in 2022?

Prices are the result of the balance between supply and demand. The demand for single-family homes has been strong over the last 18 months. The supply of houses available for sale was near historic lows. However, there’s some good news on the supply side. Realtor.comreports:

“432,000 new listings hit the national housing market in August, an increase of 18,000 over last year.”

There will, however, still be a shortage of supply compared to demand in 2022. CoreLogicreveals:

“Given the widespread demand and considering the number of standalone homes built during the past decade, the single-family market is estimated to be undersupplied by 4.35 million units by 2022.”

Yet, most forecasts call for home price appreciation to moderate in 2022. The Home Price Expectation Survey, a survey of over 100 economists, investment strategists, and housing market analysts, calls for a 5.12% appreciation level next year. Here are the 2022 home appreciation forecasts from the four other major entities:

Price appreciation is expected to slow in 2022 when compared to the record highs of 2021. However, it is still expected to be greater than the annual average of 4.1% over the last 25 years.

Bottom Line

If you owned a home over the past year, you’ve seen your household wealth grow substantially, and you’ll see another nice boost in 2022. If you’re thinking of buying, consider buying now as prices are forecast to continue increasing through at least next year.

In today’s real estate market, low inventory and high demand are driving up home prices. As many as 54% of homes are getting offers over the listing price, based on the latest Realtors Confidence Index from the National Association of Realtors (NAR). Shawn Telford, Chief Appraiser at CoreLogic, elaborates:

This home will not disappoint w/ its soaring 23” ceiling, large beams, varied ceiling heights, & wall of windows that looks out over the massive deck & reinforced bulk head pond. Amenities in this 4 bed, 4 bath home with SUN-ROOM, LOFT, and OFFICE are numerous.The kitchen features a 2 drawer Dishwasher, DOUBLE OVEN with warming tray, triple sink w/ disposable, ISLAND w/ hot water tap, sink, & disposable, you will love the POT filler over the gas 5 burner stove, wine cooler, ice maker, and slab granite on the island, large snack bar that sits 6. You have more than enough storage with the large walk in pantry, upper and lower cabinets and pull out drawers, large closets everywhere to be found. In the master, you and yours will have additional privacy w/ separate baths & walk in closets. Over-sized laundry, separate cabinet areas & utility sink along with a garage sink gives you additional comfort & care with all your laundry & outside needs. EASY maintenance w/ ceramic tile throughout most of the home, & hardy plank siding on the exterior. Nice 8 FT. doors, upscale light fixtures, fans, and hardware finish off the details of this custom-built home WITH post tension slab. If you like to entertain, the complete open flow of the home with the massive deck allows for any type of occasion that you have in mind, and everyone will enjoy the built BOSE speaker system both inside and outside the home. This home has it ALL and completes its comforts w/2. 15K generators that will keep your home up and running. The two attic entrances are floored for ample storage, along with an outside storage and LARGE workshop area. One One more perk is the parking area for any travel trailer with full hook ups with a 30 /50 amp & dump station. Now all that sits on 3.727 acres in a non-flood and never flooded CUSTOM BUILT HOME! If you are looking for privacy & luxury in the country you you must Drive out and Take A TOUR today

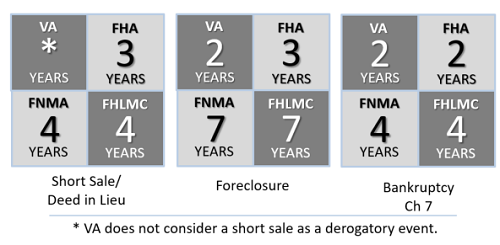

“How long do we have to wait to qualify for another mortgage” is the question concerning people who’ve had a foreclosure, short sale or bankruptcy.The loan types for the new loan will differ in amounts of time to heal credit scores based on the event.

The following chart is meant to be a general guide for how long a person might have to wait. During this waiting period, it’s important that the person be current on all payments and maintains a history of good credit.

A recommended lender can give you specific information regarding your individual situation and can make suggestions that will improve your ability to qualify for a mortgage. This process should be started before looking at homes because of the time constraints listed here can vary based on current requirements and possible extenuating circumstances of your case.

We want to be your personal source of real estate information and we’re committed to helping from purchase to sale and all the years in between. Call us at (225) 291-1234 for lender recommendations.

If you haven’t heard of a CLUE report, it has nothing to do with the table game searching for a murderer. It is a report showing the insurance claims on your home and car for the past five to seven years.

This database is used by insurance companies to evaluate risks and determine rates. C.L.U.E. stands for Comprehensive Loss Underwriting Exchange. Rates can be increased not only due to legitimate claims but data entry errors also. Sometimes, simply asking a question without filing a claim can be logged as a claim.

For that reason, similar to verifying the accuracy of your credit report, it is important to check out the CLUE report on your home and car. The reports are free and there is a process for correcting mistakes.

An interesting and sometimes costly surprise occurs during the home buying process. The claim experience of the prior seller could impact the price of the premium of the new buyer. For that reason, you can ask for a copy of the CLUE report on the home you’re interested in buying prior to writing a contract.

This home will not disappoint w/ its soaring 23” ceiling, large beams, varied ceiling heights, & wall of windows that looks out over the massive deck & reinforced bulk heard pond. Amenities in this 4 bed, 4 bath home with SUN-ROOM, LOFT, and OFFICE are numerous.The kitchen features a 2 drawer Dishwasher, DOUBLE OVEN with warming tray, triple sink w/ disposable, ISLAND w/ hot water tap, sink, & disposable, you will love the POT filler over the gas 5 burner stove, wine cooler, ice maker, and slab granite on the island, large snack bar that sits 6. You have more than enough storage with the large walk in pantry, upper and lower cabinets and pull out drawers, large closets everywhere to be found. In the master, you and yours will have additional privacy w/ separate baths & walk in closets. Over-sized laundry, separate cabinet areas & utility sink along with a garage sink gives you additional comfort & care with all your laundry & outside needs. EASY maintenance w/ ceramic tile throughout most of the home, & hardy plank siding on the exterior. Nice 8 FT. doors, upscale light fixtures, fans, and hardware finish off the details of this custom-built home WITH post tension slab. If you like to entertain, the complete open flow of the home with the massive deck allows for any type of occasion that you have in mind, and everyone will enjoy the built BOSE speaker system both inside and outside the home. This home has it ALL and completes its comforts w/2. 15K generators that will keep your home up and running. The two attic entrances are floored for ample storage, along with an outside storage and LARGE workshop area. One One more perk is the parking area for any travel trailer with full hook ups with a 30 /50 amp & dump station. Now all that sits on 3.727 acres in a non-flood and never flooded CUSTOM BUILT HOME! If you are looking for privacy & luxury in the country you you must Drive out and Take A TOUR today

The National Association of REALTORS® reports in its 2016 Profile of Home Buyers and Sellers that 12% of all buyers paid cash for their home.

Before paying cash for a home, a buyer should decide if they might put a loan on the home in the near future. It may affect the ability to deduct the interest on a mortgage placed on the home at a later date.

Homeowners can currently deduct the interest on up to $1 million of acquisition debt which are the borrowed funds used to buy, build or improve a home. Paying cash for a home establishes acquisition debt at zero. The only deductible interest to the owner would be home equity debt which is limited to $100,000 over acquisition debt.

Paying cash certainly seems like a simple decision but it may limit a homeowner’s ability to deduct interest on a future mortgage. You can get more information about this from IRS Publication 936 or from your tax professional.

The ironic thing about people who think they can’t afford to buy a home for themselves, end up buying the home for their landlord. There are several facts that support this notion.

Mortgages, whether held by an owner-occupant or an investor, are usually amortized so that each payment reduces the principal amount owed so that the loan will be repaid totally over the term. A tenant is inadvertently retiring the landlord’s mortgage with his monthly rent.

In most cases, the mortgage payment including taxes and insurance will be lower than the rent tenants are paying. Some experts are saying that we may never again experience the incredibly low mortgage interest rates currently available.

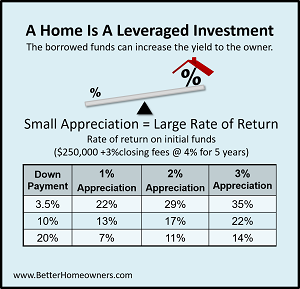

Renting precludes a person from enjoying the advantage a home has as a leveraged investment. When the borrowed funds cost less than the investment is returning, the rate of return on the down payment grows much faster. As you can see from the chart, a 2% appreciation on a home could result in big returns on the down payment. In most cases, there are very few or no alternative investments that offer homeowners similar returns.

Even if a buyer agrees with all of these things but doesn’t have the down payment or cannot qualify for a loan, they still need to investigate further. To find out exactly what types of loans are available and the specific down payment required which can be a whole lot less than 20%, they need to consult with an experienced, trusted loan professional (an Internet lender or a “BIG” bank may not be the best choice.) Call for a recommendation.

![Fact or Fiction: Homebuyer Edition [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/09/09142043/20210910-MEM-1046x1998.png)